Tecnon OrbiChem founder Charles Fryer's predictions for the chemical industry from 2022 onwards.

The chemical industry endured many problems in 2020 and 2021 but perhaps the most disruptive – which overhangs the industry still – is its logistics. Companies had become adept at sourcing molecules from where they were most economically manufactured and shipping them to where they would be converted most advantageously.

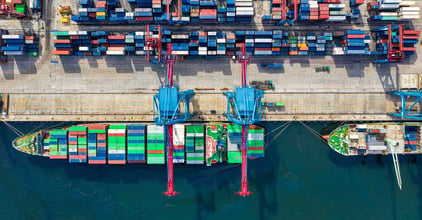

Supply chains started unraveling two years ago as problems from COVID-19 began to mount. In part, this was due to a shortage of trucks (with drivers getting ill) and disruption to rail traffic. Inland shipping issues took their toll – even water levels on the Rhine being too low, or too high. However, the major problem was delays in ocean shipping.

Ports Out, Chinese Goods Stay Home

The prime contribution to delays came from disruption at ports due to port workers off sick or in quarantine. Ships not being loaded or unloaded meant that queues of vessels waiting their turn at berths stretched out to sea. The knock-on effect was problems with containers, some were stacked waiting to be unloaded, others empty but not where needed.

Container shipping rates reached $12,000 or more for 24 tons of cargo from East Asia to the US, for example. Chinese ports in particular encountered a shortage of trucks to distribute goods due to many drivers being in quarantine. It remained a problem at Ningbo in mid-January, with the re-routing of ships to Shanghai causing congestion there too. Sometimes, ships have to skip planned stopovers at Chinese ports entirely.

Container shipping rates reached $12,000 or more for 24 tons of cargo from East Asia to the US, for example. Chinese ports in particular encountered a shortage of trucks to distribute goods due to many drivers being in quarantine. It remained a problem at Ningbo in mid-January, with the re-routing of ships to Shanghai causing congestion there too. Sometimes, ships have to skip planned stopovers at Chinese ports entirely.

But US West Coast ports have also seen queues of 60 or more ships at sea waiting to dock. To compound problems, some chemicals need refrigerated containers or temperature-controlled tanks. These delays can cause havoc. Take the MSC Flaminia’s catastrophic fire in 2012 as a harrowing reminder of the dangers of port delays. Three containers of divinyl benzene aboard the German-flagged container ship polymerized violently when the efficacy of an inhibitor expired mid-Atlantic.

Raising Inventories Over Just-in-Time Strategy

After two years of supply chain disruption, the chemical industry is considering what should be done for the future. One trend will be to work with higher inventory levels. Companies were desperate to keep plants running through 2020 and 2021. They repeatedly ramped up their price bids as stocks dwindled to secure raw materials. Never again, they say.

Undoubtedly, reliance on just-in-time (JiT) supply saves money when everything works smoothly but is a trap when it doesn’t. There will be less reliance on JiT in future. Another approach is to encourage the establishment of supplies locally and reduce reliance on suppliers halfway around the world. If this reverses a trend of the last decade or two, it amounts to reshoring an activity that had become cheaper overseas. But it’s a scenario in which both the importing and exporting countries lose out. And the world will see increased duplication of chemical plants.

Raising inventories and ditching JiT will require additional working capital, while reshoring will require investment capital. Perhaps not a huge burden with current low-interest rates, but they look likely to rise as inflation surges.

There will be many other calls on investment capital by the chemical industry as it prepares for its coming opportunities and challenges. From the transport industry’s bid to cut its carbon footprint, a full list of requirements from the chemical industry emerges:

Decarbonizing Travel and Transport

- The move to electric-powered passenger cars is well under way resulting in reduced CO2 emissions as the parc of fossil-fueled vehicles diminishes. The demand for lithium batteries is rising faster than the output of lithium by the mining companies. Therefore, improved methods of direct lithium extraction from minerals such as spodumene are urgently needed.

- Electric railway engines with onboard batteries may be the next development, with first steps now being taken in their manufacture. More powerful designs of batteries than the lithium-based variety are being worked on, which will increase the mileage between recharging.

- Hydrogen fuel and fuel cells offer an alternative to battery-driven electrification in the effort to deliver zero carbon emission trucks and buses. Today's hydrogen is mostly made from fossil fuels. Steps are being taken, however, towards the production of ‘green’ hydrogen through the electrolysis of water using solar- or wind-generated electricity.

- If green hydrogen can be made cheaply enough, it can be combined with negative cost CO2, even captured from the air, to make fuels. That sounds like science fiction, but some researchers have already achieved success at experimental levels.

- Ocean-going ship propulsion is almost exclusively through fossil fuel use at present, mostly bunker oil. Having struggled to reduce sulfur emissions in 2021, the marine industry will not relish having to reduce CO2 emissions too. One route being trialed is to use ammonia as the fuel in modified marine two-stroke engines. Ammonia as a fuel has its problems – chiefly its toxicity. Ensuring the safety of crew, port workers – and cruise passengers one day – will be the major challenge.

- Prospects for powering aircraft electrically with batteries on board are remote because of the weight of current battery types. Using hydrogen – whether compressed or cryogenic – involves the same weight disadvantage. There is no alternative to kerosene jet fuel for the foreseeable future. If air travel is to survive, chemists will have to find means of creating carbon-neutral jet fuel. The way is already clear, namely the generation of synthesis gas from carbonaceous matter and converting it to Sustainable Aviation Fuel. The most plausible candidates for suitable carbonaceous matter are forest residues and municipal waste. An alternative route is the conversion of agriculture-based ethanol to kerosene. These methods are considered sustainable since they start from raw materials regarded as carbon neutral.

The chemical industry will be actively employed in helping the transport industry meet the goals of zero net carbon emissions by 2050. Much capital investment will be needed, though this will be shared with the transport and fuel industries.

On this journey to a carbon-neutral transport system, interest rates will be carefully followed...

Sign up for our blog to get insights like these delivered right to your inbox.

10 Essential Steps for Navigating the Methanol Market