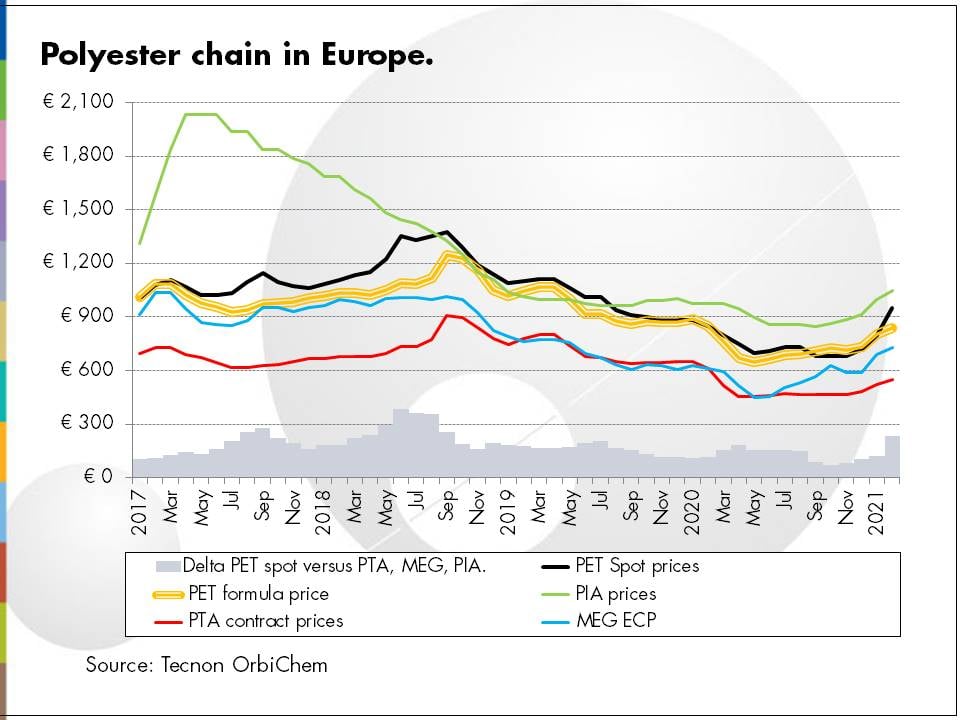

The concerns relating to availability of PET in December, as European producers struggled to bring plants back online following scheduled maintenance, continued into January and has been accelerated in early February. There are still major issues with availability and cost of freight from Asia, which has meant that Asian PET, but also PTA and PIA is currently not widely available and uncompetitive on a delivered basis. This encouraged or forced buyers in the polyester chain to rely more on European sources, as it has been the case for PET, PTA, MEG and PIA.

In addition, reduced inventories in the European chain, extended turnaround outages and unexpected output constraints have created tight markets for PET, MEG, PTA and PIA in recent weeks, leaving a number of European PET producers struggling to secure sufficient product to operate plants. This, together with increases in crude oil Brent values and higher prices in Asia, has resulted in higher contract prices and margins for main feedstocks and PET in Europe, as well as much higher quotes for spot values.

For PET, these issues on the PET supply side of the equation are set against a background of low inventory levels through the downstream pipeline and sharply rising raw material costs. There has therefore been a rush to replenish stocks in anticipation of further significant price rises which has, at least temporarily, caused a surge in demand. It is not yet clear how strong the demand is at a consumer level given the latest restrictions in hospitality, travel and the stay at home guidance in place across much of Europe. Operating rates of the industry in Europe have clearly improved and are assessed around 80% only limited by the lack of enough feedstocks to operate. Freely negotiated PET values firmed rapidly during the second half of January, with deals around €1000/ton ddp confirmed in February and differences depending on the region, volume and commercial relationship. Supply constraints and maximized contract volumes have provided limited spot business, with agreements for new or additional contract volumes confirmed with deltas of around €250/ton on main raw materials, PX and MEG.