Today’s MEG scenario reflects the different and difficult dynamics that will continue to impact and shape markets in the coming months and years.

- All the expected, new glycol capacities - in the US through 2019, but also in early 2020 in China and Malaysia - have now started up and are operational.

- Lower demand due to COVID-19 is only worsening structural overcapacity of MEG. The glycol market will need to find a new equilibrium in 2020 through rationalisation in the form of shut-downs and reduced operating rates.

- The importance of competitive feedstock and where new units are located on the cash cost curve will drive this process. However, trade barriers, logistics as well as local and idiosyncratic circumstances will define how each producer in each region justifies operation or rationalisation.

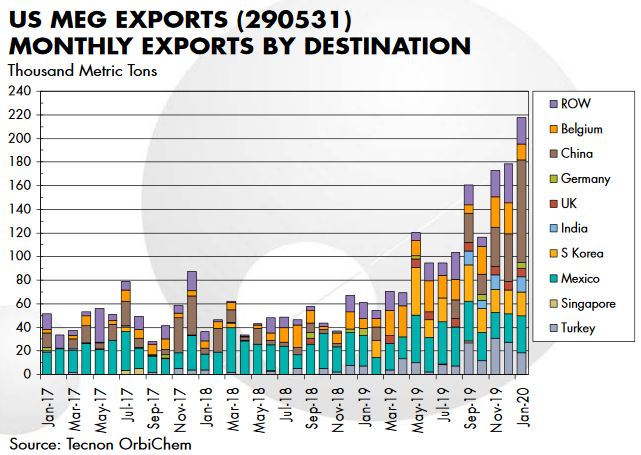

China continues to be the main MEG consumer, with imports of just under 10 million tons in 2019. Three new petroleum-based glycol units have just started up in China, adding 2.5 million tons of new capacity in 2020. With the stated aim of reducing its import dependency (aided by coal-based MEG production), 2020 should see lower MEG imports into China.

Two main regions, North America (in particular the USA) and the Middle East, will continue to compete for exports markets in order to secure additional volumes - in most cases at the expense of local production in importing areas.

All glycol units in the USA ran at very high output levels in 2019. Competitive feedstock continues to be a key factor supporting glycols manufacture in the country, allowing exports to grow and justifying the high operating rates. Brent values at low levels ($35/bbl ) have decreased the previous competitiveness of producers in the US compared to naphtha-based producers.