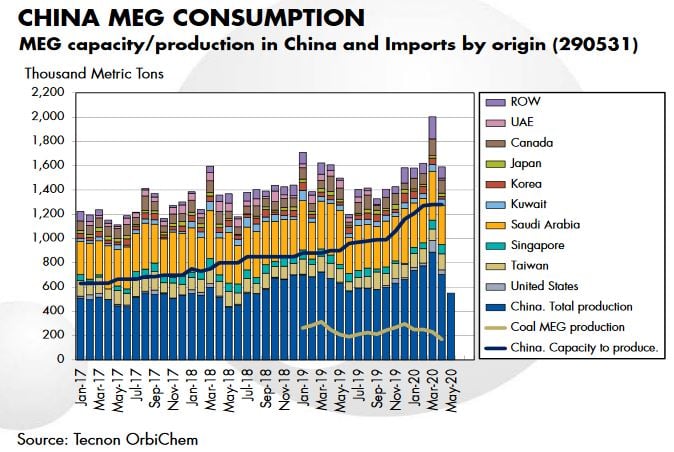

Since the start of 2020, we have seen Brent crude oil futures fall from just under $70/bbl to $23/bbl. MEG values followed, plummeting from $608/ton to $350/ ton cfr in early April. And although there has been a rebound, relatively low Brent crude prices of around $40/bbl still prevail, along with very low MEG values in all the regions.

Lower crude oil prices are generally welcomed by the chemical industry, as not only feedstock costs but usually also energy costs are reduced. However, particularly for MEG, non-petrochemical feedstocks have become more important in recent years. Coal-MEG, as well as bio-MEG has become the focus of much interest, with new capacity and production in the case of coal-to-MEG, and expectations and projects in the case of bio-MEG.

- Coal-MEG producers (with a relatively unchanged feedstock cost) are facing big losses forcing them to reduce operating rates and review their feasibility in the new crude oil and MEG scenario.

- Bio-MEG remains the highest cost and highest price option. Although the main driver for bio-MEG continues to be related to sustainability, the wider price gap relative to the fossil-based alternative forces clients to take stock of the value of its use.

Producers of MEG using all feedstock slates have been affected by overcapacity and low glycol prices, as well as different cash-cost positions given the new Brent crude oil values. Region plays its part in this change but the profitability of producers using two less traditional feedstocks has been challenged by the low-cost crude oil environment.